Soft and Hard Hammer Endorsements in CGL: What Contractors Actually Pay For

In Commercial General Liability, a "soft/hard hammer" endorsement is a behavioral tool. Carriers use it to change how contractors operate.

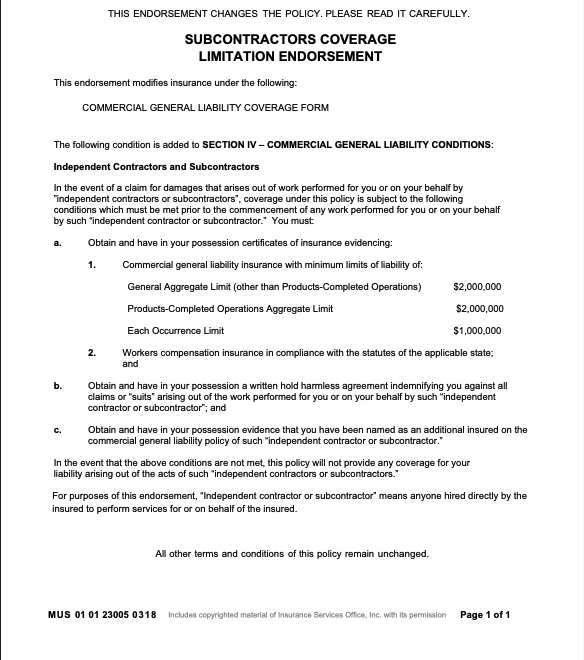

It sounds administrative. It also saves you money on premium. But these endorsements show up constantly, and most people don't understand what they're actually agreeing to. I've attached an example for reference.

What Is a Subcontractor Warranty Endorsement?

Subcontractor warranty endorsements (what many call soft or hard hammers) are designed to modify how an insurance organization operates.

It asks you to carry certain paperwork as a requirement to getting the full benefit of your policy in the event of a claim. If you miss a requirement, then you're staring at a deductible that can cripple a business (soft hammer) or have your coverage negated (hard hammer).

That's how this becomes an endorsement that impacts the behavior of the policyholder/insured.

Why Carriers Use Them

From the carrier's perspective it makes sense. These endorsements push insureds to tighten up their paperwork:

- Maintain certificates of insurance

- Execute contracts

- Track hold harmless provisions

- Confirm limits

- Stay organized

In theory, it improves risk management, but here's what often gets misunderstood:

This endorsement doesn't just tweak and cheapen coverage. It rewires your workflow.

The Real Cost of a Cheaper Premium

It forces you to build, adopt, or buy administrative infrastructure. You either invest in consultants (I've seen engagements around +/- $20k, though capacity is usually limited on the consultants' side), or you build it internally. And that means real payroll, software, benefits, etc. For many small to mid-sized contractors, a functional risk management setup can easily run north of $100k annually.

That's the trade.

You can accept the cheaper policy with the subcontractor warranty endorsement, but then you must properly equip your team to meet every condition, every time.

Or you can pay more for a policy that removes it. I've seen cases where the delta was $30k. That's not insignificant, but neither is building an internal compliance engine just to preserve coverage you thought you already had.

It's More Than Paperwork

The hammer clause is more than just paperwork.

It's about whether your organization is structured to survive the paperwork.

Before choosing the cheaper quote, ask yourself:

Are we pricing the policy, or pricing the operational burden that comes with it?

Where Hammer Endorsements Actually Show Up

Most organizations and brokerages say that they do not accept placements that put soft or hard hammer clauses in their GC's policies.

But hammer endorsements frequently appear with subcontractors.

These endorsements, while not common with general contractors, don't really cause damage there. But do they cause damage on the subcontractor substrata that the GC hires?

The Takeaway

Take one rule away from this: cheaper insurance doesn't mean you got a deal. You just bought less coverage. And if you're relying on outsourced reviews to catch these endorsements, make sure they actually understand what they're looking at.