Insurance Has Entered an AI Arms Race, and Most of the Market Doesn't Even Realize It Yet

At InsurTech Chicago's recent summit on AI in the insurance workplace, a moderator posed a simple question to a panel of senior executives from major organizations that have been leading the charge in adoption of artificial intelligence. She asked them to rate their company's AI adoption on a scale of one to three, where one meant using foundational, off-the-shelf models like ChatGPT or Copilot, and three meant maximally embedding AI into their core workflows.

Every leader on that panel proudly declared "two".

Then came the follow-up. "Can you walk us through your tech stack?"

Silence. Shuffling. A few nervous smiles. Someone eventually offered: "We mix it up. We believe in a few tools. We predominantly use ChatGPT, Copilot, and Claude."

That moment told me everything I needed to know about where commercial insurance actually stands with AI in 2026. This should concern every serious professional in this industry.

"They couldn't define a tech stack. But they were certain they were a two out of three on AI adoption."

What insurance actually uses AI for

Let's start with where Insurance is today with AI adoption.

After spending the better part of a year speaking with professionals across the P&C space (Insurance brokers, carriers, TPAs, adjusters, risk managers, consultants) the picture is remarkably consistent. The industry has embraced off-the-shelf AI tools with genuine enthusiasm. It's just applied them to a very short list of tasks:

- Summarizing and polishing emails

- Formatting Excel formulas

- Reviewing insurance policies and other documents

- Summarizing claims files

There is nothing wrong with any of these applications. They save time. They reduce friction. But calling this an AI strategy, rating yourself a two out of three, is the organizational equivalent of buying a Formula 1 engine and using it to idle in a parking lot for a food truck.

The uncomfortable truth is this: most insurance professionals are not leveraging AI.

Their employees are though. Quietly, individually, often without any formal policy, the people actually doing the work discovered these tools and started using them to survive their workload. Leadership then looked around, noticed the efficiency gains, signed an enterprise agreement with Anthropic or OpenAI, issued a press release, and declared victory!

The employees already beat them to it. And leadership is mistaking the effect for a strategy.

Three things your team gets wrong when they open ChatGPT

But here is where the employees get it wrong.

The way insurance professionals use off-the-shelf AI tools is not just limited. It's often actively counterproductive. Here are the three failure modes I encounter constantly when P&C professionals reach out to me about leveraging AI in their P&C commercial businesses.

Failure mode 1: Speed over accuracy

When you upload a 200-page policy into ChatGPT and ask it to review the whole document, it doesn't review the whole document. To generate an answer in seconds, the model prioritizes the most statistically relevant sections based on your prompt, not a comprehensive reading. It skips content. It glosses over edge cases. And then it writes a confident, well-formatted summary of its incomplete analysis. These are not obvious errors. They are appealing, coherent, plausible-sounding gaps. Which in an industry that focuses on Errors and Omissions - these are the most dangerous kind.

Failure mode 2: Training on your clients' data

In a survey I am currently conducting across P&C organizations, roughly 40% of respondents have never turned off the setting that allows AI models to use their documents and prompts to improve the general model. All of these organizations go through rigorous procurement. That means client policies, claims files, proprietary coverage analyses are uploaded directly into tools that may be using them to train publicly accessible systems. The professionals doing this are not malicious. They simply do not know. And that is a systemic failure of the organizations deploying these tools without governance.

Failure mode 3: No guardrails, no principles, no accountability

Off-the-shelf AI is, by definition, built for everyone. It has no understanding of your specific policy language, your carrier relationships, your clients' risk profiles, or the legal and regulatory standards your work is governed by. It will hallucinate with the same polished confidence whether it is right or catastrophically wrong. Without custom guardrails, system-level principles, and verification layers, you are not deploying AI, you are deploying liability. Only now, it's got a branded deal made with massive insurance organizations.

The caviar company, the top-5 broker, and a $32 million wake-up call

A case study from the field

A caviar company was positioned as the front-runner on two contracts, a $23 million deal and a $9 million deal, what would have been the two largest deals in their company's history.

They lost both in the span of a month.

Not on price nor on product quality nor on reputation. They lost because the organizations on the other side of those negotiations had changed how they vet vendors using Vendor Insurance Vetting AI technology. They were no longer reviewing certificates of insurance. They were reviewing the policies themselves. And when they did, they found a total product exclusion buried in the commercial general liability coverage.

That exclusion had been sitting on those policies for multiple years. Through renewals, through growth, through a dozen conversations about coverage a top-5 broker with a team of sixty professionals across multiple lines had never flagged it. Not once. Funny enough, none of the quoting carriers during the marketing exercises even picked up on it for an account that has had 0 losses in 22 years. (But hey, at least they presented competitive rates!)

Here are the results:

- $32M in combined deal value lost by the caviar company in just one month where they were the favorite

- $10M+ in premium the broker will lose by end of week

- $275K Brokerage fee gone; for a policy review that takes minutes with the right AI, or even a properly trained entry employee

This is not a story about negligence, at least not in the obvious sense. It is a story about what happens when an industry decides that thorough policy review is a function of headcount rather than intelligence. It is a story about what happens when the institutional answer to a knowledge problem is "hire more people."

The review that would have caught that exclusion, the review that would have saved both the caviar company's contracts and the broker's relationship, takes minutes with the right AI-powered tool. Not a summary. Not a skim. A comprehensive, structured, governed analysis of every line.

The market is no longer asking for certificates. It is asking for the policy. Is yours clean?

Why insurance is falling behind, and why it isn't entirely its own fault

Let me be direct about something the industry rarely wants to say out loud: insurance professionals do not have a creativity problem. They have a demonstration problem. They don't know what AI could do for them because nobody has shown them.

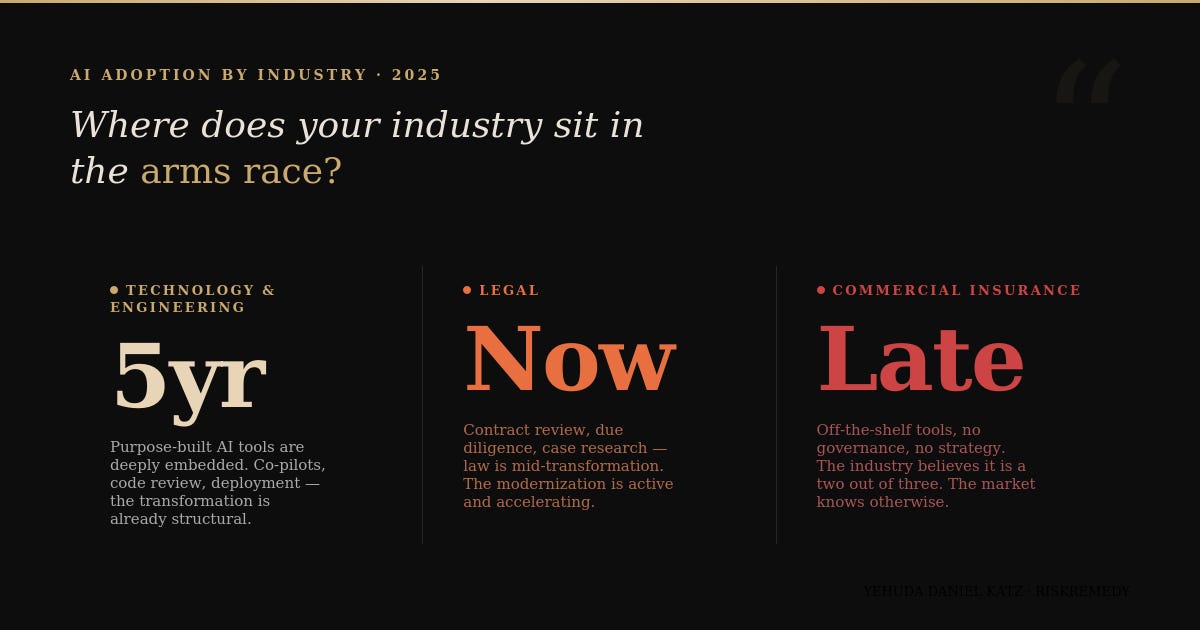

Software engineers have had AI co-pilots for years. The tools are deeply embedded, purpose-built, and iterating fast. Lawyers are in the middle of a genuine transformation right now (contract review, due diligence, case research) all being rebuilt around intelligence rather than billable hours some great solutions include Parambil (AI-powered platform for Tort Law) and Docsum - AI Contract Review and Negotiation Platform.

And then there is insurance. Where the same executives who claim a two out of three on AI adoption are, in the next breath, asking how many full-time employees they should hire to handle their growing book of business.

Part of this is the industry's fault. There is a cultural resistance to technological disruption in commercial insurance that is almost theological in its consistency. Change is slow. Relationships are everything. "That's how we've always done it" is not a joke, it is actual strategic reasoning in many organizations.

But the larger fault lies with the technology providers themselves. I wrote recently about why insurtech has failed to gain meaningful traction despite operating in an industry that is, in theory, perfectly suited for AI disruption. The reason is straightforward: for the better part of fifteen years, the majority of insurtech startups promised gold to insurance professionals, took their money, and delivered ash. The startups closed the doors, and the insurance professionals now had a reduced budget that would have been safer to deploy for an extra FTE. The trust deficit that created is real, documented, and entirely deserved.

Insurance professionals are not naive. They have been burned enough times to be skeptical of every new technology pitch. The problem is that their skepticism has calcified into a posture that rejects even the tools that genuinely work.

The largest carriers will announce agentic AI at their next conference, then ask how many FTEs you need to service your account. We have accepted this contradiction without comment.

The arms race is not coming. It is already here.

While the major players hold conferences and announce AI partnerships they do not yet know how to use, something quieter and more consequential is happening at the margins of this market.

Smaller, more agile organizations (brokers, MGAs, Startups using their own products, boutique risk consultants) are beginning to offer services that simply were not economically possible two years ago. A risk analysis that a top-5 broker quoted at $50,000 and six weeks of turnaround? Some operators are delivering a comparable product for a few thousand dollars with a response time measured in hours, not months, while offering a whole toolkit for other workflows.

Risk managers who have spent years being told that comprehensive policy review was a luxury they couldn't afford are now finding it within reach. The barriers were never technical. They were economic. AI has dismantled them methodically and steadily.

The organizations that understand this, that are quietly redeploying headcount from administrative and operational functions into genuine revenue-generating roles, are not making announcements. They are just winning deals that their larger, less nimble competitors assume are still theirs to lose.

One organization we have been working with entered this process expecting to hire six or seven additional people to handle policy review volume. Instead, they procured RiskRemedy for policy and document review, and then they redeployed that headcount entirely into profit centers. They did not cut costs. They did not downsize. They simply stopped needing people to do work that a well-governed AI system does better, faster, and with greater consistency.

That is what actual AI adoption looks like. Not a ChatGPT enterprise license. Not a two out of three on a panel. A fundamental reallocation of human intelligence toward the work that only humans can do.

The honest question for your organization

On that scale of one to three: where three means AI is genuinely, structurally embedded in how your organization delivers value, where do you actually sit?

Not where leadership believes you sit. Not what the press release said. Where are you, operationally, today?

Because the market you are competing in is no longer grading on a curve.

What comes next

The arms race has started. The large organizations can afford to move slowly, for now. Scale is its own protection. But the window in which size alone insulates you from the competitive pressure of smaller, AI-native operators is closing faster than most of the industry recognizes.

The next wave is not ChatGPT for emails. It is purpose-built, governed, domain-specific intelligence, systems that understand the difference between an occurrence and a claims-made policy, that flag total product exclusions before they become $32 million lessons, that let brokers spend their time building client relationships instead of manually comparing policy schedules.

Some organizations will move first. They will take deals they never imagined they could win. They will offer services at price points that permanently alter client expectations in this market.

The rest will hold their next conference and announce that they are moving to agentic AI. And then they will ask you how many full-time employees you need.

The choice about which kind of organization you want to be is, for now, still yours to make.