A Warning to Those Who Only Review Certificates of Insurance

I was reading a policy for someone as a favor recently. This is a warning to those of you that only review certificates of insurance.

I recently reviewed a commercial package policy for a specialty distributor with stable operations and $10 million in revenue. The red flag to me was that the policy only had $2,600 for a premium. They've worked with the same broker for over a decade.

Their Certificate of Insurance was clean in every way that typically matters. In fact, a major wholesale retail giant just "vetted" them and approved their insurance because:

- The limits looked right.

- The carriers were reputable.

Nothing was out of place. Every entity was listed as additional insureds and certificate holder.

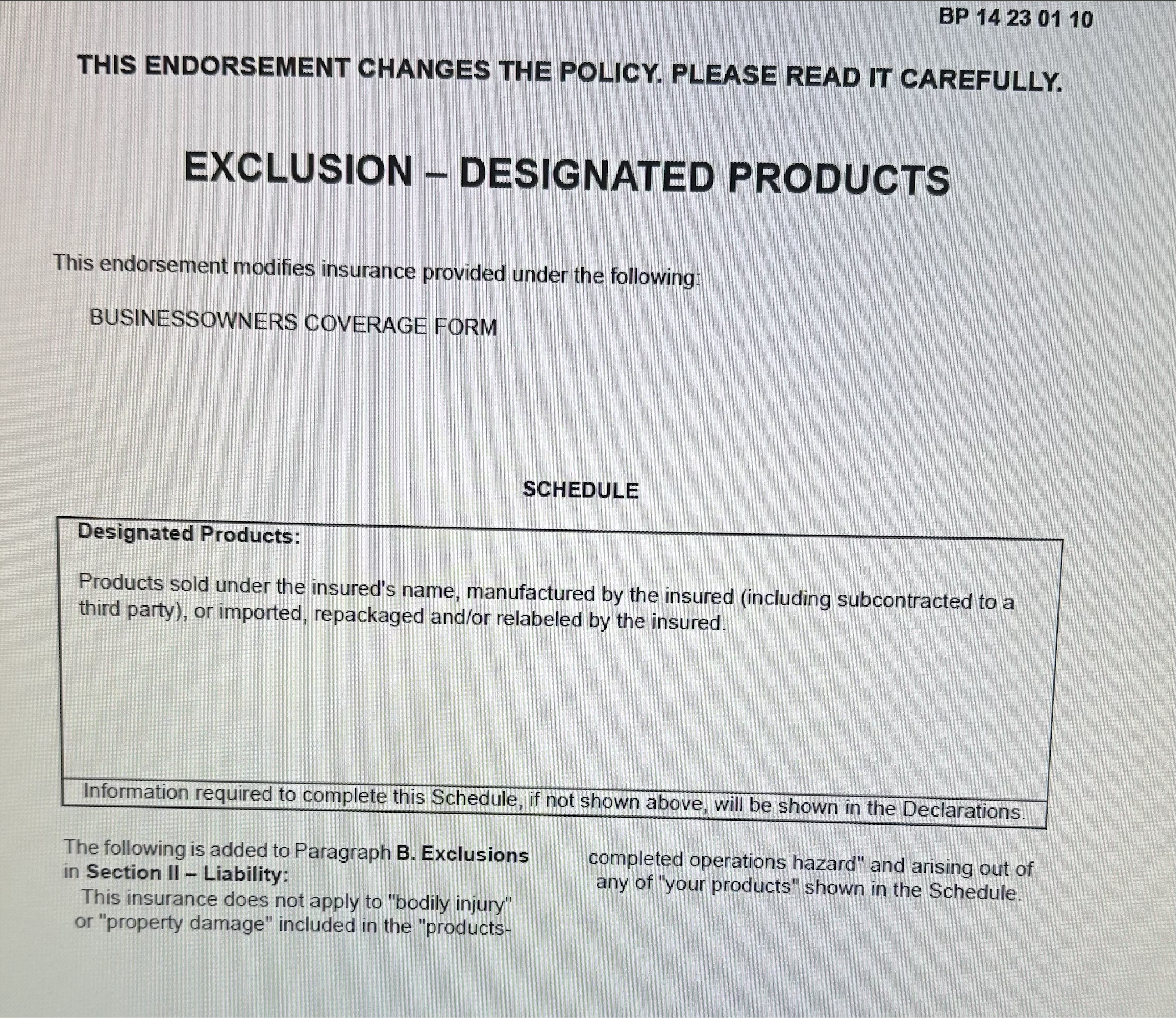

The Problem Appears Only After Reading the Policy

Buried deep in the document was an endorsement titled "Exclusion - Designated Products." The schedule excluded products sold under the insured's name, including those imported, repackaged, or relabeled by the insured.

That description matched the company's core operations exactly. In short, they were paying for a paper that gave them no coverage at all.

With a few lines of boilerplate language, the policy removed Products-Completed Operations coverage for the very activity generating revenue. The rest of the policy read normally. The declarations page raised no obvious flags. The premium, while modest, only became concerning in hindsight.

The Certificate did not disclose this exclusion. It couldn't have. Certificates do not grant coverage, amend policy language, or override endorsements. They summarize what they can—and omit what they must.

A Decade of Unnoticed Risk

What was most striking was not the exclusion itself, but how long it had gone unnoticed. The broker relationship spanned eleven years. The operations were consistent. Yet no one had surfaced that the policy effectively excluded the business it was meant to insure.

This isn't a failure of effort. It's a failure of process.

Across insurance and risk management, we've trained ourselves to treat certificates as substitutes for coverage analysis, and many insurance professionals have forgotten what it means to read an insurance policy. We check cleanliness, confirm limits, and move on. Under time pressure, that shortcut becomes the system.

But risk doesn't live on certificates. It lives in endorsements.

When Exclusions Trigger

When an exclusion like this triggers, there is no debate. The carrier doesn't argue. The certificate doesn't help. The risk simply returns to the insured. And this is the warning to those of you that only collect certificates and judge them for their numbers. You are still holding the risk if you don't read the policy.

That reality is why we built RiskRemedy—not to replace human judgment, but to make policy review unavoidable, repeatable, scalable, and seamless.

The Lesson

- A clean certificate doesn't mean you're covered.

- If the policy hasn't been read, the risk is already yours.